You filed your tax return expecting the usual refund, or at least to break even, only to discover you owe taxes this year. The shock hits hard when staring at a tax bill that seems to come out of nowhere, especially when you feel like nothing in your financial situation has changed.

The reality is that even when your life feels stable, subtle shifts in tax laws, income patterns, withholding amounts, or personal circumstances can significantly impact your tax liability.

In this blog post, our team at Lewis CPA will explore why you might owe taxes when nothing seemingly changed, and how proactive tax planning can help you avoid unwelcome surprises next year.

Did Nothing Change? Common Contributing Factors.

Even seemingly minor or indirect changes can significantly impact your tax liability. What feels like "no change" to you might involve several subtle shifts that collectively create a higher tax bill. Let's explore the most common culprits behind unexpected tax debt so you know what to expect.

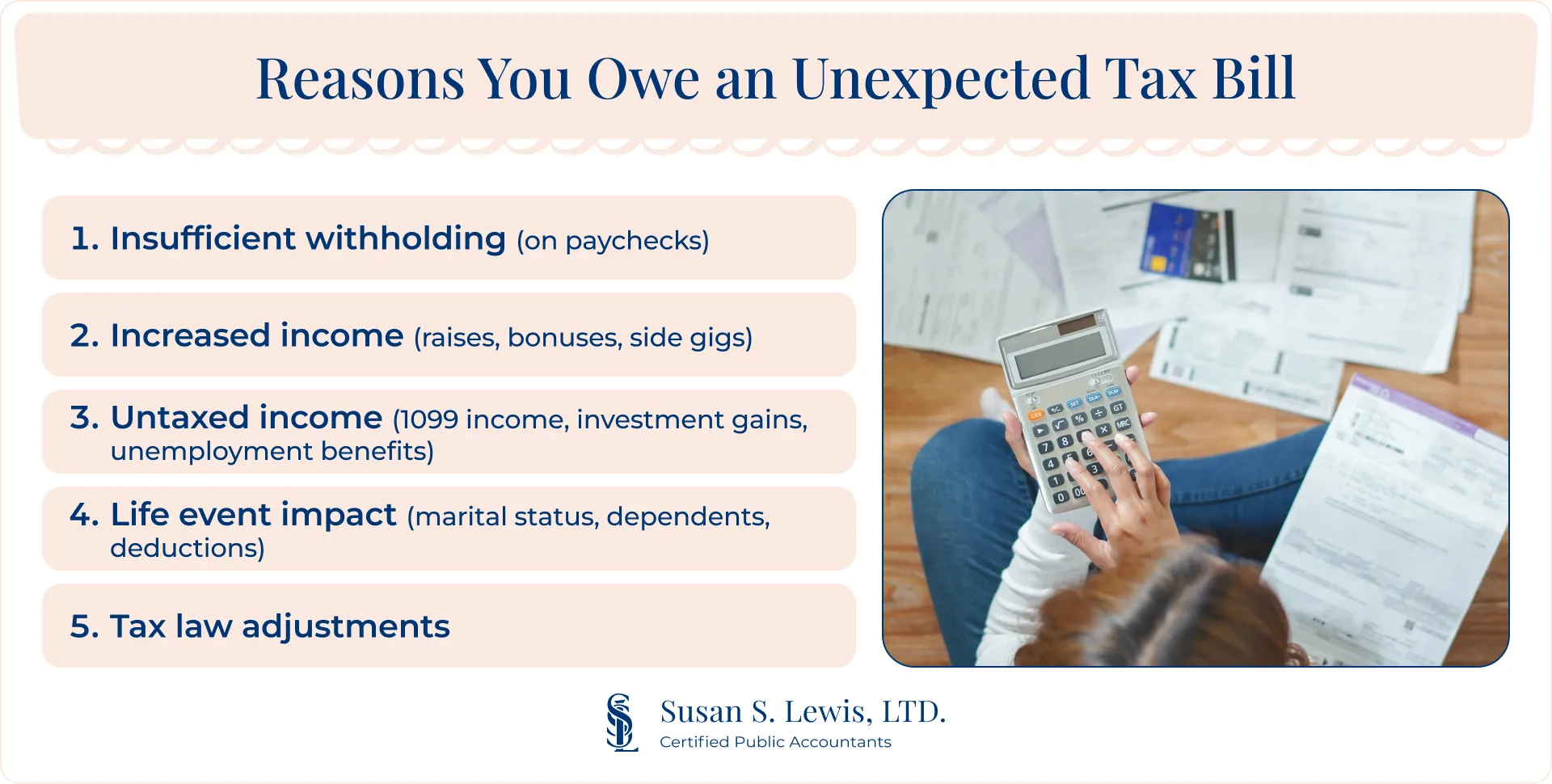

Insufficient Withholding

This is often the biggest reason taxpayers owe money at tax time. Your W-4 form dictates how much tax is withheld from your paycheck, and even small miscalculations can lead to owing taxes when you expected a refund.

Here are some common scenarios that cause insufficient withholding:

- Multiple jobs: Each employer withholds taxes based only on their income, not your total taxable income from all sources.

- New job or job change: Starting a new job mid-year often means your initial W-4 doesn't accurately reflect your full-year income.

- Incorrect W-4 setup: Claiming too many allowances or deductions results in less tax withholding throughout the year.

- Bonuses or irregular income: These payments may not have sufficient taxes withheld, creating a gap in your tax payments.

- Changes in filing status: Getting married or divorced affects how much tax should be withheld from your pay periods.

Changes in Income (Even Small Ones May Matter)

Has your income changed, even a small amount? Even modest income increases can push you into a higher tax bracket or reduce your eligibility for valuable tax credits. Remember, tax brackets are progressive, but additional income can still impact your overall tax liability.

Income changes that commonly trigger tax debt:

- Salary raises: Small increases can push you into higher tax brackets or reduce credit eligibility.

- Side gigs and freelance work: This 1099 income usually doesn't have taxes withheld, requiring estimated tax payments.

- Investment gains: Selling stocks, cryptocurrency, or other assets creates taxable capital gains.

- Unemployment benefits: These are taxable income, and many people don't have taxes withheld from payments.

- Retirement account withdrawals: Distributions from traditional IRAs or 401(k)s count as taxable income.

- Self-employment income: Requires paying both employee and employer portions of Social Security and Medicare taxes.

Life Changes Impacting Credits and Deductions

Life changes can dramatically affect your eligibility for tax credits and deductions, even when your income is relatively stable. Taxpayers are often caught off guard by these changes because they seem unrelated to tax obligations.

Common life changes that affect tax liability include:

- Loss of dependents: Children aging out of eligibility for the child tax credit or other dependent-related benefits.

- Marital status changes: Getting married or divorced significantly impacts filing status, deductions, and available credits.

- Homeownership changes: Paying off your mortgage or selling a home impacts interest deductions and capital gains.

- Itemized vs. standard deduction shifts: Changes in deductible expenses might make itemizing less beneficial.

- Loss of specific credits: Education credits, energy efficiency credits, or other benefits may expire or no longer apply.

Tax Law Changes (Federal and Illinois Specific)

Tax laws change regularly, and modifications to tax brackets, standard deduction amounts, or available tax breaks can impact your tax liability even when your situation remains stable.

Recent changes affecting Illinois taxpayers:

- Illinois personal exemption adjustments: The amount increased from $2,425 for 2023 to $2,775 for 2024.

- New Illinois tax credits: Including the Volunteer Emergency Worker Credit and updates to existing credits.

- Federal tax bracket modifications: Small adjustments that might not be immediately obvious but impact your tax calculation.

- Credit phase-out changes: Income ranges for certain tax credits may have been adjusted, affecting eligibility.

- Expiration of tax benefits: Some credits or deductions may have expired or been restricted since last year.

Errors or Miscalculations

Sometimes owing taxes simply results from human error or miscalculations during tax preparation. Even with modern tax software, mistakes can happen and create unexpected tax liability.

Common errors that lead to tax debt:

- Simple math errors: Manual calculations or data entry mistakes during tax preparation.

- Overlooked income sources: Forgetting to include certain 1099 forms or other income sources.

- Incorrect information entry: Miskeying numbers from W-2s, 1099s, or other tax documents.

- Job change coordination issues: When changing employers mid-year, withholding coordination might not be seamless.

- Missing deductions or credits: Failing to claim eligible tax benefits that could reduce your tax liability.

What to Do If You Owe Taxes This Year

We understand that owing taxes can feel overwhelming, but don't panic — owing taxes is manageable with several viable solutions. The key is taking action as soon as possible to understand your options and prevent the problem from worsening.

#1. Review Your Tax Return

Before making any payments or payment arrangements, thoroughly review your tax return to ensure it’s accurate. Sometimes, simple corrections significantly reduce the amount you owe.

- Verify all income sources: Double-check that all W-2s, 1099s, and other income documents are accurately reported.

- Confirm deductions and credits: Ensure you've claimed all eligible tax benefits, including retirement contributions and education credits.

- Compare with previous years: Look for unusual differences that might indicate errors or missed opportunities.

- Check mathematical calculations: Even with tax software, manual errors can occur during data entry.

- Consider overlooked deductions: Review potential deductions you might have missed, such as charitable contributions or business expenses.

#2. Understand Your Options for Payment

If you owe taxes and can't pay the full amount by the tax deadline, you have several options. Don’t ignore it; instead, address your tax debt promptly.

- Pay in full immediately: If possible, pay the entire amount to avoid additional interest and penalties.

- IRS installment agreement: Set up a payment plan to pay your tax debt over time with manageable monthly payments.

- Offer in compromise: In cases of financial hardship, potentially settle your tax debt for less than the full amount owed.

- Request penalty relief: If you have a good compliance history, you might qualify for penalty abatement.

- Temporary delay: If you're experiencing severe financial hardship, the IRS might temporarily delay collection.

#3. Adjust Your Withholding for Next Year

The most effective way to avoid owing taxes next year is to adjust your tax withholding and payment strategy. This proactive approach helps ensure you're paying enough taxes throughout the year.

- Update your W-4: Submit a new Form W-4 to your employer to increase withholding based on your current tax situation.

- Use the IRS Tax Withholding Estimator: This online tool helps determine the appropriate withholding amount.

- Make estimated quarterly payments: Essential for self-employed individuals or those with irregular income.

- Consider additional withholding: If you have multiple income sources, request extra withholding from your primary job.

- Work with a tax professional: Get personalized advice on optimizing your withholding strategy for your situation.

How Lewis.cpa Can Help Illinois Taxpayers

At Lewis.cpa, we have local expertise and understand the unique aspects of Illinois tax law, from personal exemption amounts to state-specific credits and deductions. We’re here to guide you through this topic. Here’s how we can help.

- Personalized tax situation analysis: We dig deep into your circumstances to identify the root causes of your tax debt.

- W-4 optimization: Our team can help you correctly complete your W-4 to ensure proper withholding throughout the year.

- Estimated tax payment guidance: We advise on appropriate quarterly payments for self-employed individuals and those with irregular income.

- Maximum deductions and credits: We ensure you're not missing any eligible tax breaks, especially those specific to Illinois residents.

- Tax law change navigation: We keep clients updated on federal and Illinois tax law changes that could impact their situation.

- IRS and state tax issue resolution: Professional assistance with tax notices, payment plans, and Offer in Compromise negotiations.

Whether you're dealing with capital gains taxes, complex investment income, or multi-state tax obligations, our team at Lewis CPA is always ready to help you navigate these challenges while protecting your financial interests.

Plan for a Smoother Tax Season Next Year

If you want to avoid owing taxes next year, the key is proactive planning and regularly reviewing your tax situation throughout the year. Don't wait until tax season to think about your tax liability — work with a qualified tax professional to monitor your withholding, make estimated payments when necessary, and adjust your tax strategy as your situation changes.

Remember that owing taxes isn't necessarily a crisis, but it requires prompt attention and proper planning. Lewis.cpa is here to help Illinois taxpayers navigate these challenges and develop comprehensive strategies for long-term tax success. With us, taxes don’t have to be stressful or complicated. Contact us today to discuss your situation and learn how we can help you achieve a smoother, more predictable tax season next year.