Founding Father Benjamin Franklin once said, "Nothing is certain except death and taxes." If you’re a high-income earner, your biggest wins usually come from planning, not last-minute scrambling. The goal is to lower taxable income where you can, keep investment income tax efficient, and avoid “stealth taxes” that quietly inflate your total tax liability. While no one likes to pay taxes, there are strategies to reduce them, such as hiring a personal tax accountant like ours at Lewis.cpa.

Before we dive in, remember that tax laws change, and your financial situation matters. The strategies below are meant to be actionable, but the right mix depends on your income sources, state income tax exposure, business structure, and timing.

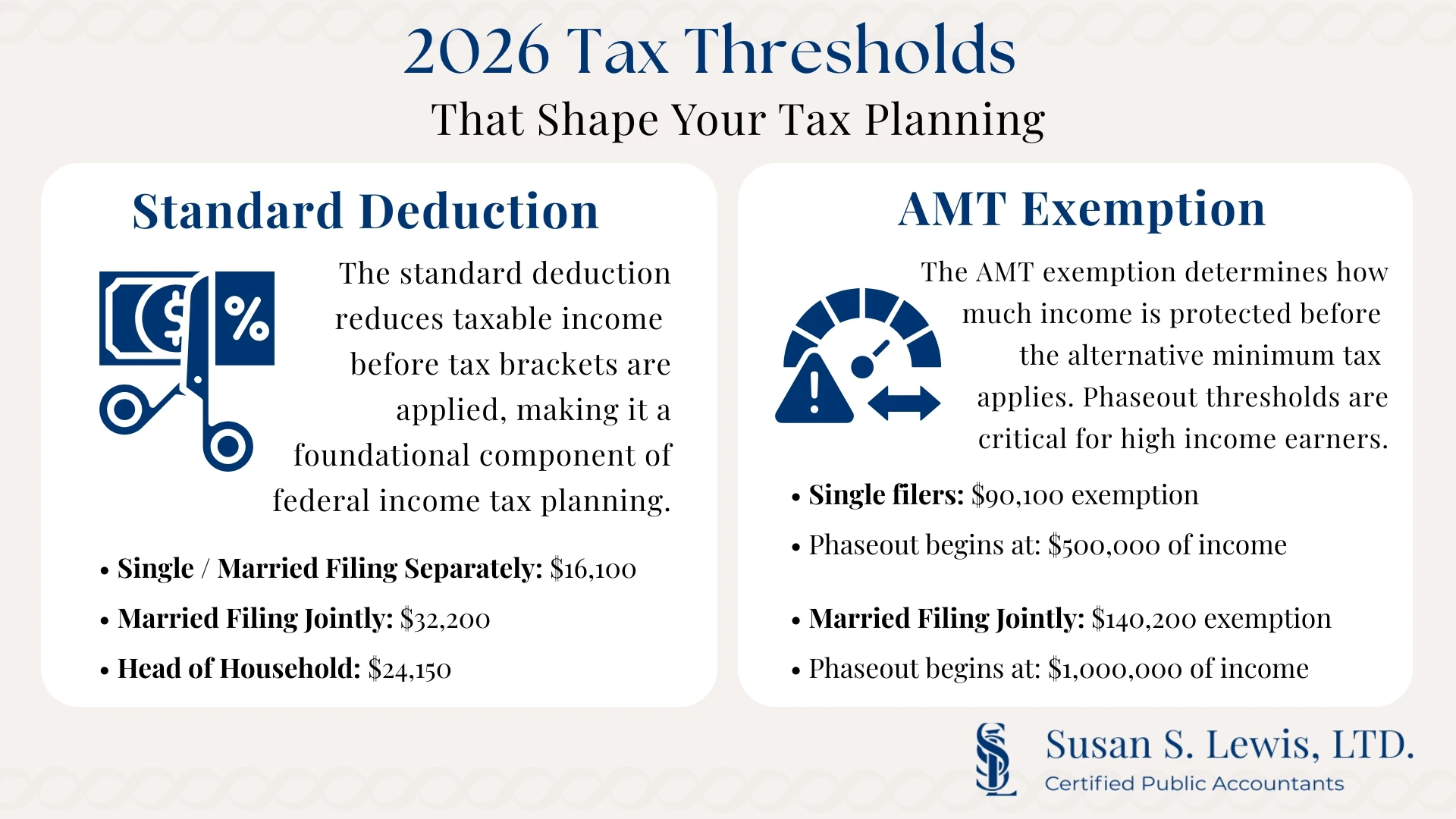

2026 Baseline Numbers You Should Know

Tax planning starts with the correct year’s thresholds. For tax year 2026, the IRS inflation adjustments include a higher standard deduction and updated AMT exemption amounts.

- Standard deduction (2026): $16,100 single/MFS, $32,200 MFJ, $24,150 HOH.

- AMT exemption (2026): $90,100 single (phaseout begins at $500,000) and $140,200 MFJ (phaseout begins at $1,000,000).

These numbers matter because they change whether you itemize deductions, how much benefit you get from certain tax breaks, and whether a strategy that worked last tax year still works now.

What Actually Drives Taxes for High-Income Earners?

Tax planning can get confusing when it focuses on labels instead of mechanics. For high-income earners, the size of the tax bill is determined by how income is categorized and layered.

These four factors are typically the most important:

- Ordinary income vs. capital gains: Wages, bonuses, and business income are generally taxed at ordinary income rates, while long-term capital gains may receive different treatment. The mix between the two often has a bigger impact than total income alone.

- Exposure to payroll and Medicare taxes: High earners often pay more than just federal income tax. Payroll taxes, self-employment tax, and the Additional Medicare Tax can materially increase total tax liability when income crosses certain thresholds.

- Adjusted and modified adjusted gross income (MAGI): Many deductions, tax benefits, and contribution limits phase out as adjusted gross income or modified adjusted gross income increases. Even when tax rates stay the same, these phaseouts can quietly raise the effective tax rate.

- Timing of income and deductions: When income is recognized and when deductions are taken can shift income between tax years and tax brackets, which directly affects the current tax bill.

Once you know which type of income is pushing your taxes higher, you can choose strategies that actually reduce taxable income rather than only reshuffling it.

Strategy 1: Reduce Taxable Income with the “Cleanest” Levers First

The best tax-saving strategies for high-income earners usually start with the tools that directly reduce taxable income without complicated structuring.

Max Out Workplace Retirement Contributions

If you have access to a 401(k), 403(b), or governmental 457 plan, this is often the most straightforward way to reduce taxable income at the federal level while building long-term tax efficiency.

For 2026, the IRS announced that the elective deferral limit is $24,500, and the general age-50+ catch-up is $8,000 (so many high earners can contribute up to $32,500, depending on plan rules).

Action steps:

- Payroll setup: Increase your deferral percentage early in the tax year so you don’t miss the contribution limits.

- Bonus timing: If you receive large bonuses, confirm how your plan handles deferrals on bonus compensation so you don’t underfund.

- High earners note: Some catch-up rules changed for 2026 planning and may require Roth treatment in certain situations, so plan administration is important in this case.

Use the IRA Strategy Correctly

IRAs can still play a role, but the value depends on income limits, existing balances, and how you’re coordinating retirement money across accounts.

For 2026, the IRS release on retirement adjustments notes an IRA limit increase. It also discusses how Roth IRA contribution thresholds change by year.

If you’re considering Roth IRA contributions, you should also be aware of income limits. Recent reporting on 2026 thresholds reflects the phaseout ranges for Roth IRA eligibility, which MAGI drives.

Strategy 2: Health Savings Account Planning for Tax-Free Growth

An HSA is one of the most tax-advantaged accounts available when you’re eligible through a high-deductible health plan. It can reduce current taxable income, grow tax-free, and come out tax-free when used for qualified medical expenses.

For calendar year 2026, the IRS set HSA contribution limits at $4,400 (self-only) and $8,750 (family), and it defines the HDHP parameters that control eligibility.

Action steps:

- Eligibility check: Confirm you qualify under the HDHP rules before contributing, especially if you changed coverage mid-year.

- Practical play: If cash flow allows, treat the HSA as a long-term account and pay qualified medical expenses out of pocket while saving receipts, so you can preserve tax-free growth.

Strategy 3: Itemized Deductions That Still Move the Needle

Many high earners assume itemized deductions will always beat the standard deduction, but that’s not automatically true in 2026. This is especially the case if you moved, changed property taxes, or your state and local taxes changed.

SALT Is No Longer “Stuck” at $10,000 in 2025–2029

For taxpayers who itemize deductions, the IRS explains the combined SALT deduction limit is $40,000 ($20,000 if married filing separately), subject to a modified adjusted gross income limitation and not reduced below $10,000.

Action steps:

- If you pay high property taxes and state income tax: Re-run itemizing every tax year, because SALT may now be a meaningful lever again.

- If your MAGI is high: Plan for the phase-down mechanics so you don’t overestimate the deduction.

Charitable Deductions with a Better Structure

Charitable giving can be a powerful tax reduction strategy, but it’s most effective when you match the tool to the goal.

Common high-income approaches:

- Donor-advised funds: Useful when you want to “bunch” charitable deductions into one tax year while granting over time.

- Appreciated assets: Donating appreciated securities can reduce capital gains tax exposure while still supporting the deduction strategy (subject to substantiation and AGI limits).

#cta_start

Get Answers Before Decisions Become Expensive

Small timing and structure decisions can have a large tax impact when income levels are high.

#cta_end

Strategy 4: Control Capital Gains and Investment Income More Intentionally

For many high-income earners, the tax bill isn’t only about wages. It’s often driven by capital gains, dividends, and other investment income that stacks on top of ordinary income.

Capital Gains Tax Depends on Holding Period and Income Character

The IRS is clear that net short-term capital gains are taxed as ordinary income, while long-term gains are treated differently.

Action steps:

- Holding period planning: If a sale is close to one year, timing may shift the character of income.

- Gain stacking: Plan large sales in years when other taxable income is lower so you don’t accidentally push yourself into a higher tax bracket.

NIIT Is a Common “Surprise” Tax for High Earners

The Net Investment Income Tax adds 3.8% on certain net investment income when MAGI exceeds statutory thresholds ($250,000 MFJ, $200,000 single/HOH, $125,000 MFS).

Action steps:

- If you’re selling a business interest, real estate, or a concentrated position: Model NIIT before you sell.

- If you’re deciding between wage income and investment income: Remember, NIIT generally applies to investment income, not wages, so character matters.

Additional Medicare Taxes and Payroll Taxes

High earners can also owe the 0.9% Additional Medicare Tax when Medicare wages and/or self-employment income exceed thresholds ($250,000 MFJ, $200,000 others, $125,000 MFS).

If you’re self-employed, self-employment tax (Social Security and Medicare) is a separate planning layer that impacts total tax liability and cash flow.

Action steps:

- W-2 earners: Watch withholding and bonus timing so you don’t get caught with an unexpected balance due at tax season.

- Business owners: Coordinate compensation planning, payroll taxes, and deductions, so you’re not optimizing one area while losing in another.

Strategy 5: Tax-Efficient Investing Tools

There are legitimate ways to be more tax efficient, but they’re not “set it and forget it.” The right approach depends on AMT exposure, your state income tax situation, and what’s in taxable vs. tax-advantaged accounts.

Municipal Bonds Are Useful, But AMT Can Matter

IRS Publication 550 notes that some tax-exempt interest can be a tax preference item and may be subject to AMT depending on the bond type and issuance details.

That doesn’t mean municipal bonds are “bad.” It means they need to be selected intentionally, especially for many high-income earners who are closer to AMT territory.

Mutual Funds vs. ETFs and Ongoing Tax Drag

For taxable accounts, fund structure and turnover can affect annual distributions. In return, this affects taxable income and your current tax liability. Publication 550 is a good reference point for how investment income and expenses are treated.

Action steps:

- If you hold actively managed mutual funds in taxable accounts: Watch year-end distributions.

- If you’re building tax-efficient investments: Consider asset location (what goes in taxable vs retirement accounts) alongside product selection.

Strategy 6: Business Owner Planning and Advanced Tools

If you have business income, the planning conversation changes because you can influence timing, deductions, and income character more directly. This is where entity planning and business deduction strategy can reduce taxable income significantly, but it must be coordinated with payroll taxes and long-term goals.

Examples that often come up for high earners:

- Entity and compensation planning: Balancing W-2 wages, distributions, and reasonable compensation requirements.

- Timing deductions: Planning large purchases, retirement contributions, and expense timing across the tax year.

- Qualified Small Business Stock: Potentially valuable for capital gains planning, but it’s heavily rules-based and documentation-sensitive.

A Simple Planning Checklist for the Tax Year

This repeatable process helps high-income earners stay proactive rather than reactive.

Quarterly check-ins:

- Income tracking: Review taxable income, capital gains, and ordinary income exposure.

- Deduction tracking: Track state and local taxes, property taxes, and charitable deductions if you plan to itemize.

- Account funding: Confirm contribution limits for retirement accounts and health savings account contributions are on pace.

- Tax projections: Run a projection that includes NIIT and Medicare taxes so you can avoid surprises.

Let Lewis CPA Handle Your Tax Planning

Effective tax planning for high-income earners requires more than knowing the rules. It requires ongoing execution: tracking income throughout the tax year, applying the correct tax strategies at the right time, coordinating deductions and investments, and ensuring every move complies with current tax laws. When done correctly, this work can significantly reduce taxable income, improve long-term tax efficiency, and prevent costly mistakes that surface during tax season.

Lewis.cpa provides full-service tax planning and tax preparation for high-income earners who want their taxes handled correctly and efficiently. We manage the strategy, calculations, filings, and compliance so you don’t have to worry about shifting rules, missed opportunities, or unexpected tax liability. If you’re ready for experienced professionals to handle your tax planning, contact us today.

#cta_start

Have Your Tax Strategy Built and Managed

We handle the planning, calculations, and filings so your tax strategy is implemented correctly from start to finish.

#cta_end